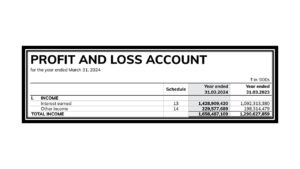

Income of Banking Company – Interest Income

Income of Banking Company

Interest income and Fee income, the two are the Banking Company’s operating source of income. Banking Companies primarily accept deposits (in the form of Term deposits (FD/RD), saving a/cs, current a/cs) from public at a certain percentage (%) and thereafter lend these deposits in the form of loans/limits at a certain percentage (%) to individuals/entities in need of money to cater to their personal or business fund requirements.

Below are the types of income earned by a Banking Company and the classification and reporting of it in its Profit and Loss Account:

Interest Income/Interest Earned

Includes:

i. interest and discount on all types of loans and advances like

- cash credit,

- demand loans,

- overdrafts,

- export loans,

- term loans,

- domestic and foreign bills purchased and discounted (including those rediscounted)

ii. interest on debt instruments (including Government securities),

iii. overdue interest and also penal interest,

iv. interest subsidy, etc., if any, relating to such advance/bills.

Note:

- Dividend on equity/ preference shares is other operating income.

- Interest on advance income tax, etc. are to be considered as miscellaneous income.

Other Operating Income

Income earned from regular activities of banks other than from the core operations of lending and investing of funds, which yield interest income. It includes :

i. commission, exchange and brokerage (such as commission on bills for collection, commission/exchange on remittances/transfers, commission on LCs / guarantees,

ii. processing charges,

iii. syndication fees,

iv. credit/debit card fee income,

v. locker rent,

vi. commission on government business,

vii. brokerage on securities,

viii. fee on insurance / mutual fund referral and banking service charges),

ix. profit on exchange transactions (revaluation gains/losses on forward foreign exchange contracts and other derivative contracts, premium income/expenses on options, etc),

x. dividends from subsidiaries and joint ventures abroad/ in India.

Income from Off-Balance Sheet Operations

Income earned from contingent facilities like :

i. fee income earned for issue of LCs, BGs, acceptances, endorsements and committed lines of credit) and

ii. positive marked to market (MTM) valuations of derivative transactions or gains recorded on derivative transactions due to favourable movements of market variables (such as yields, exchange rates).

Non-operating income

Non-operating income is income earned by banks from sources other than their core/ regular activities and which are not their regular source of income, for e.g.

i. profit (and losses) on sale of fixed assets/ HTM category investments,

ii. revaluation of HTM category investments,

iii. recovery of written-off assets, etc.

Norms for Recognizing Income in Profit and Loss Account

Income Recognition Policy

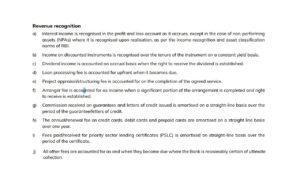

i. The policy of income recognition has to be objective and based on the record of recovery. Therefore, the banks should not charge and take into income account interest on any NPA. This will apply to government-guaranteed accounts also.

ii. However, interest on advances against

- Term Deposits,

- National Savings Certificates (NSCs),

- Kisan Vikas Patras (KVPs) and

- life insurance policies

may be taken to income account on the due date, provided adequate margin is available in the accounts.

iii. Fees and commissions earned by the banks as a result of renegotiations or rescheduling of outstanding debts should be recognised on an accrual basis over the period of time covered by the renegotiated or rescheduled extension of credit.

iv. In cases of loans where moratorium has been granted for repayment of interest, income may be recognised on accrual basis for accounts which continue to be classified as ‘standard’.

Reversal of income

i. If any advance, including bills purchased and discounted, becomes NPA, the entire interest accrued and credited to income account in the past periods, should be reversed if the same is not realised. This will apply to Government guaranteed accounts also.

ii. If loans with moratorium on payment of interest (permitted at the time of sanction of the loan) become NPA after the moratorium period is over, the capitalized interest, if any, corresponding to the interest accrued during such moratorium period need not be reversed.

iii. In respect of NPAs, fees, commission and similar income that have accrued should cease to accrue in the current period and should be reversed with respect to past periods, if uncollected.

Appropriation of recovery in NPAs

i. Interest realised on NPAs may be taken to the income account provided the credits in the accounts towards interest are not out of fresh/ additional credit facilities sanctioned to the borrower concerned.

ii. In the absence of a clear agreement between the bank and the borrower for the purpose of appropriation of recoveries in NPAs (i.e. towards principal or interest due), banks should adopt an accounting principle and exercise the right of appropriation of recoveries in a uniform and consistent manner.

Interest Application

On an account turning NPA, banks should reverse the interest already charged and not collected by debiting Profit and Loss account and stop further application of interest. However, banks may continue to record such accrued interest in a Memorandum account in their books. For the purpose of computing Gross Advances, interest recorded in the Memorandum account should not be taken into account.

Example of norms practically used by Banks in India

Reference Material – Master Circular – Prudential norms on Income Recognition, Asset Classification andProvisioning pertaining to Advances

Career in Banking – Current Job Openings

Finance Banking Accounting Auditing Costing

Leave a Reply