Micro, Small and Medium Enterprises Development (MSME) Act

Brief on Micro, Small and Medium Enterprises Development (MSME) Act, 2006

Priority Sector Lending

RBI has issued guidelines on Priority Sector Lending (PSL) vide its circular1 in which they had categorized the below sectors under Priority Sector:

i. Agriculture ii. Micro, Small and Medium Enterprises iii. Export Credit iv. Education v. Housing vi. Social Infrastructure vii. Renewable Energy viii. Others

Therefore, the MSME sector falls under Priority Sector Lending.

Objective

Central Govt. to facilitate the promotion and development and enhance the competitiveness of MSME units (particularly of the micro and small enterprises) by way of development of skills in the employees, management, and entrepreneurs, provisioning for technological degradation, marketing assistance or infrastructure facilities and cluster development to strengthen backward and forward linkages.

Providing Credit Facilities: The policies and practices in respect of credit to the MSME units shall be progressive and RBI to ensure a timely and smooth flow of credit to such enterprises, minimizing the incidence of sickness.

Govt should ensure the preference policies in respect of procurement of goods and services, produced and provided by micro and small enterprises, by its Ministries or departments, or its aided institutions and PSUs.

Important Definitions (Section 2)

2(b) Appointed Day means the day following immediately after the expiry of the period of 15 days from the day of acceptance or the day of deemed acceptance of any goods or any services by a buyer from a supplier.

Explanation – For this clause

(i) The day of acceptance means:

(a) the day of the actual delivery of goods or the rendering of services

or

(b) where any objection is made in writing by the buyer regarding the acceptance of goods or services within 15 days from the day of the delivery of goods or the rendering of services, the day on which such objection is removed by the supplier.

(ii) the day of deemed acceptance means: where no objection is made in writing by the buyer regarding the acceptance of goods or services within 15 days from the day of the delivery of goods or the rendering of services, the day of the actual delivery of goods or the rendering of services.

2(d) Buyer means whoever buys any goods or receives any services from a supplier for consideration;

2(e) Enterprise means an industrial undertaking or business concern or any other establishment engaged in the manufacture or production of goods pertaining to any industry specified in the First Schedule to the Industries (Development and Regulation) Act, 1951 or engaged in providing or rendering of any service or services.

2(f) Goods means every kind of movable property other than actionable claims and money;

2(g) Medium Enterprise means given in Table below.

2(h) Micro Enterprise means given in Table below.

2(m) Small Enterprise means given in Table below.

2(n) Supplier means a micro or small enterprise, that has filed a memorandum with the authority referred to in sub-section (1) of section 8.

Classification of enterprises (Section 7)

- Composite criteria of Investment and Turnover shall apply.

- If a Unit crosses (upward) either of the limits of Investment or Turnover then the said Unit will be placed in the next higher category.

- If a Unit crosses (downward) both the limits of Investment & Turnover then the said Unit will be placed in a lower category.

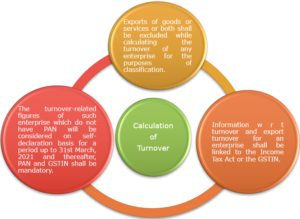

- All units with GSTIN listed against the same PAN shall be collectively treated as one enterprise and the turnover and investment figures for all of such entities shall be seen together and only the aggregate values will be considered for deciding the category as MSME.

Calculation of investment in Plant and Machinery (P&M) or equipment:

Calculation of Turnover:

8. Memorandum of micro, small and medium enterprises.

Click here to verify Udyam Registration Certificate (URC)

Delayed payments to Micro and Small Enterprises (Sections 15, 16 & 17)

15. Liability of buyer to make payment: Where any supplier supplies any goods or renders any services to any buyer, the buyer shall make payment therefor on or before the date agreed upon between him and the supplier in writing or, where there is no agreement in this behalf, before the appointed day.

Provided that in no case the period agreed upon between the supplier and the buyer in writing shall exceed forty-five days from the day of acceptance or the day of deemed acceptance.

16. Date from which and rate at which interest is payable: Where any buyer fails to make payment of the amount to the supplier (as required under section 15) the buyer shall, notwithstanding anything contained in any agreement between the buyer and the supplier or in any law for the time being in force, be liable to pay compound interest with monthly rests to the supplier on that amount from the appointed day or, as the case may be, from the date immediately following the date agreed upon, at three times of the bank rate notified by the RBI.

17. Recovery of the amount due: For any goods supplied or services rendered by the supplier, the buyer shall be liable to pay the amount with interest thereon as provided u/s 16.

Disclosures in Financial Statements (Section 22 & 23)

Balance Sheet:

(i) Under the heading “Equity and Liabilities”, in para (4), for “(b) Trade payables” the following shall be disclosed, namely:—

(b) Trade Payables:

(A) total outstanding dues of micro-enterprises and small enterprises and

(B) total outstanding dues of creditors other than micro-enterprises and small enterprises

(ii) Under the heading Notes: General Instructions for preparation of Balance Sheet”, in para 6, after sub-para F the following shall be inserted, namely:—

Trade Payables

The following details relating to Micro, Small and Medium Enterprises shall be disclosed in the notes:

(a) the principal amount and the interest due thereon (to be shown separately) remaining unpaid to any supplier at the end of each accounting year.

(b) the amount of interest paid by the buyer in terms of section 16 of the MSME Development Act, 2006, along with the amount of the payment made to the supplier beyond the appointed day during each accounting year.

(c) the amount of interest due and payable for the period of delay in making payment (which have been paid but beyond the appointed day during the year) but without adding the interest specified under the MSME Development Act, 2006.

(d) the amount of interest accrued and remaining unpaid at the end of each accounting year; and

(e) the amount of further interest remaining due and payable even in the succeeding years, until such date when the interest dues above are actually paid to the small enterprise, for the purpose of disallowance of a deductible expenditure u/s 23 of the MSME Development Act, 2006.

23. Interest not to be allowed as a deduction from income:

Notwithstanding anything contained in the Income-tax Act, 1961 (43 of 1961), the amount of interest payable or paid by any buyer, under or in accordance with the provisions of this Act, shall not, for the purposes of computation of income under the Income-tax Act, 1961, be allowed as deduction.

24. Overriding effect

The provisions of sections 15 to 23 shall have effect notwithstanding anything inconsistent therewith contained in any other law for the time being in force.

27. Penalty for contravention of section 8 or section 22 or section 26:

(1) Whoever intentionally contravenes or attempts to contravene or abets the contravention of any of the provisions contained in sub-section (1) of section 8 or sub-section (2) of section 26 shall be punishable—

(a) in the case of the first conviction, with a fine which may extend to INR 1,000; and

(b) in the case of a second or subsequent conviction, with a fine which shall not be less than rupees one thousand but may extend to INR 10,000.

(2) Where a buyer contravenes the provisions of section 22, he shall be punishable with a fine which shall not be less than INR 10,000.

Micro, Small and Medium Enterprises Development (MSME) Act, Micro, Micro Small and Medium

Other Articles

Finance Banking Accounting Auditing Costing

0 Comments on “Micro, Small and Medium Enterprises Development (MSME) Act”